If anyone in the drug and alcohol addiction recovery community had any doubts about what the Republican Party’s repeal of the Affordable Care Act might do, despite the series of sobering headlines over the years, the headlines suddenly “got real” in January of 2017.

That’s when it was announced that more than 40,000 Americans would die from a repeal of Obamacare, a figure calculated by reversing studies that show how many lives are saved when people are granted basic medical insurance.

The number stands out from the thousands of headlines over the political season, throughout a long, strange presidential campaign, about what then candidate Donald Trump’s pledge to repeal President Obama’s signature accomplishment might do to gut the Affordable Care Act. But those headlines mostly had to do with dollars and cents – or, more accurately, about a billion dollars here and a billion dollars there. And those numbers tended to change day to day, as pundits and think tanks compare one option to another with the goal posts moving constantly.

It was still dire news. One mid-January report from the Commonwealth Fund concluded that the repeal of Obamacare would mean the loss of $140 billion in federal funding for health care in 2019 alone, leading to the loss of 2.6 million jobs, most of those from the private sector.

A third of those jobs, needless to say, would be in the health care sector, the report says, adding that the aggregate gross state product across the country would stand to lose $2.6 trillion in reduced business output from 2019 to 2023 – a span of five years. “States and health care providers will be particularly hard hit by the funding cuts,” the report says.

More alarming, the Commonwealth Fund says the gutting of the ACA will go right at the heart of the addiction and recovery community’s funding in that, “a likely strategy is to repeal two key elements of the health reform law: the insurance premium tax credits and the expansion of Medicaid eligibility.” In other words, the two most critical provisions that helped the poor or the near-poor afford insurance would be the most likely place where cuts are made.

The reason for this assumption points straight to the Republican party’s lack of a solid replacement option for Obamacare. Congressional Republicans with only repeal in their minds and no plan for what comes next have to point to something tangible whenever those nagging reporters and the vociferous constituents who show up at Town Hall meetings across the country ask them what to expect next.

To curtail a rising public relations disaster they have on their hands, Republicans are pointing to a repeal plan from 2015 that was vetoed by President Obama. That plan was really a lame duck unto itself, a test case that had no case at all, as it aimed for the heart of the president’s signature and storied piece of legislation. With that option, says the Commonwealth Fund, “millions lose their insurance, hospitals and other providers would see their uncompensated medical care costs soar by $1.1 trillion from 2019 to 2028, and they would experience major revenue losses as well.”

The Repeal Cuts Deep

A repeal, however, cuts even deeper than that because funding tends to stimulate the economy no matter where it is originally spent. The Commonwealth Fund predicts that gains will be reversed throughout the economy, including drops in state and local tax revenues. In addition, like sprinkling salt on the wound, Republican governors, like all well-intended public servants, tend to assert their priorities at every turn, which means, like art during a recession, programs to help the poor are where Republicans quickly look for cuts rationalizing that basic services, such as roads and law and order need to be maintained even during the lean years.

This highlights what would tend to be an obvious factor for those in the health care community and any of their patients who suffer from mental health disorders or addiction, namely: Every battle is a personal one. The numbers of fatalities, dollars spent and jobs lost or gained stand as a surreal backdrop to the immediate problem of getting a client through the day clean and sober or trying to secure housing, a meal, clothing, transportation or child care on an ongoing basis for someone in need, especially when that someone is plagued by the urge to return to a life of risking everything on the next fix.

Headlines tell the stories with candid precision: “A Recent Spike In Cocaine Overdose Deaths Has Been Linked To The Opioid Epidemic,” reads a BuzzFeed headline, noting the phenomenon is “largely due to dangerous opioids like Fentanyl,” according to a December 2016 report from the American Public Health Association.

“Maryland reports another sharp spike in overdose deaths,” a Washington Post headline from mid-September 2016 declares. And then there are the local spikes in otherwise calm communities, such as Ithaca, New York, or Louisville, Kentucky, which are suddenly besieged by a Fentanyl supply in the area.

“Middlesex County Sees Spike In Fatal Overdoses,” says a Boston.com report that relays the news of 33 overdose fatalities in the community in a little over a month – from March 1, 2016 to April 7, 2016 – including 19 heroin-related deaths, all occurring in a county with a population of 1.6 million.

Middlesex Attorney General Marian Ryan said that state police had responded to 65 overdose deaths through April 7 of that year, which was the same as the total of all overdose deaths from 12 months of 2012. In a plea to community members at a Friday press conference, Ryan all but declared a state of emergency for the county. “We want to be saving lives this weekend,” Ryan said, noting, “this is a public health crisis. This is a community crisis. We need the community to step forward and help us.”

Meanwhile, across the country, states are looking at different repeal scenarios based mostly on whether or not their governors accepted the Medicaid expansion component of the health care reform or not.

That provision, which the Supreme Court ruled optional in a 5-4 vote in June 2012, sets up a much harder future for states that reached out for the extra help, as now they are at risk of losing that much more than the 19 states that have not adopted Medicaid expansion.

According to the Kaiser Family Foundation, states that expanded Medicaid through Obamacare had three times greater enrollment growth (36 percent to 12 percent) than states that turned their backs on the expansion option. That would tell you that most of the expected declines in coverage will be in areas of the largest growth in Medicaid, the Foundation noted in an in-depth study of the impact of the repeal.

Affects Vary State to State

Nationally, in 2015, the number of adults made eligible for insurance through Medicaid’s expansion who stood ready to lose that coverage stood at an estimated 11 million, the think tank said. “However, the scope of coverage losses will vary state to state depending on how the repeal is implemented.”

The common denominator across state lines is the fear that a repeal will mean no coverage or reduced coverage across the board, especially among those newly covered by Medicaid – a number the Kaiser Family Foundation says is expected to grow, as the trend has been towards increased enrollment and because two new states, Louisiana and Montana, have recently join those accepting the Medicaid expansion option.

Between the summer of 2013, just prior to the ACA, and September 2016, the net increases in Medicaid and in the Children’s Health Insurance Program had reached 15.7 million people, the Kaiser Family Foundation says. Another way to measure that is to look at the trend that allowed the number of uninsured among non-elderly U.S. residents – excluding foreign born and residents here illegally – from 16.6 percent in 2013 down to 10 percent by 2016 – an historic low.

When the Supreme Court ruled that states could opt out of the Medicaid extension program, the ruling further sub-divided an already complicated law. The Affordable Care Act included about 2,000 pages of legislation that tried to fill hundreds of perceived flaws in the healthcare system across the country with mandates that ranged from fast food restaurants supplying calorie counts for their meals to the right for women to choose their own reproductive health physicians – their obstetrician-gynecologists.

More pointedly for addiction recovery services, the ACA made it illegal for insurers to deny coverage for people based on their pre-existing conditions, a blanket excuse for decades that companies used to discriminate against people with either a mental health diagnosis or an addiction, frequently because those conditions often go hand in hand.

The ACA righted a long-term flaw in the healthcare laws by extending the 2008 Mental Health Parity and Addiction Equality Act that applied to private insurers to include also persons with Medicaid or anyone participating in the state or federal insurance exchanges. Add this all up and 32 million people who were previously not able to bill an insurance company for recovery services were able to do so, according to the Substance Abuse and Mental Health Services Administration – an overnight game changer for recovery in-house or out-service recovery programs.

Supreme Court Ruling Divided the Country

The Supreme Court, however, cleaved the country in two by allowing states to opt out of the Medicaid expansion and over time 19 states refused to do so, although some, like Wisconsin, carved out a hybrid system for itself, while others, like Florida, have governors who insists the new law was sold on “a lie,” as Republican Gov. Rick Scott has said.

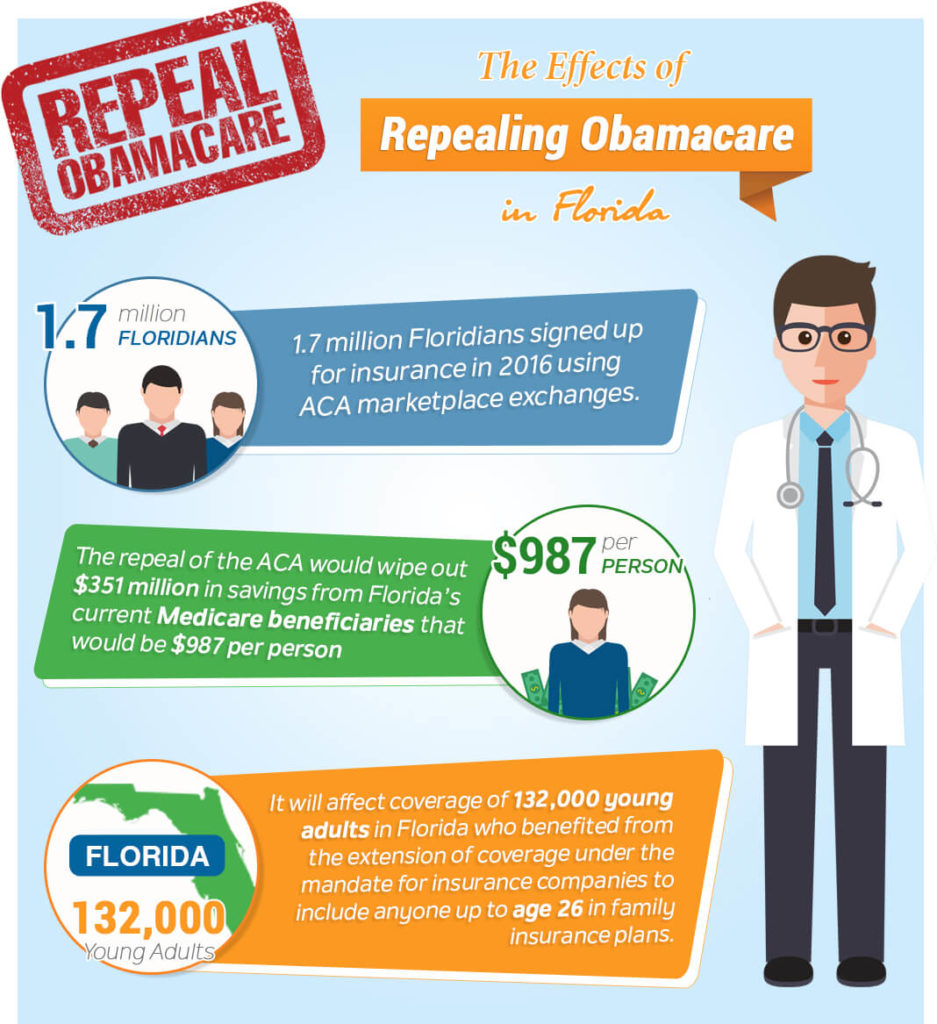

Florida itself might be most affected by the repeal of Obamacare, and not due to its lack of Medicaid expansion. According to Healthcare.gov, there were 1.7 million Floridians who signed up for insurance in 2016 using ACA marketplace exchanges, “the most of any state,” said Congressman Ted Deutch, (Fla., 22cnd District). Furthermore, says the Congressman, the repeal of the ACA would “wipe out $351 million in savings,” from Florida’s current Medicare beneficiaries – that would be $987 per person – because it would also be a setback for drug benefits covered by the law.

Deutch points out how far ranging the affects of a repeal would be. It will affect coverage of 132,000 young adults in Florida who benefited from the extension of coverage under the mandate for insurance companies to include anyone up to age 26 in family insurance plans. It would end cancer screenings and flu shots that the law provides for at no cost. “In short, repeal will return our health care system to a time when insurance companies had too much power and too often came between patients and their care,” Deutch said in an opinion piece published by the Sun Sentinel.

In Wisconsin, another state that did not opt for extending Medicaid, a so-called hybrid plan was developed. This came about as Republican Gov. Scott Walker cherry-picked his options and decided to use federal dollars not to expand Medicaid according to ACA standards (those earning up to 138 percent of the federal poverty line) but to cover adults without children who were at or below the federal poverty line itself while extending help to non-profits, health programs and insurance agencies to help state residents to participate in the federal marketplace exchanges.

As rated by the publication Politico, at least by 2013, Mississippi represented another predicament, which Politico simply related to as “a mess.” This occurred when Mississippi Insurance Commissioner Mike Chaney tried to go it alone in an effort to support a law he didn’t particularly like, despite the point that Gov. Phil Bryant offered no support for Obamacare, which was declared an impasse by the Department of Health and Human Services. The upshot of all this was that Chaney proposed to oversee ACA support for small businesses, while letting the federal government manage the individual insurance exchanges.

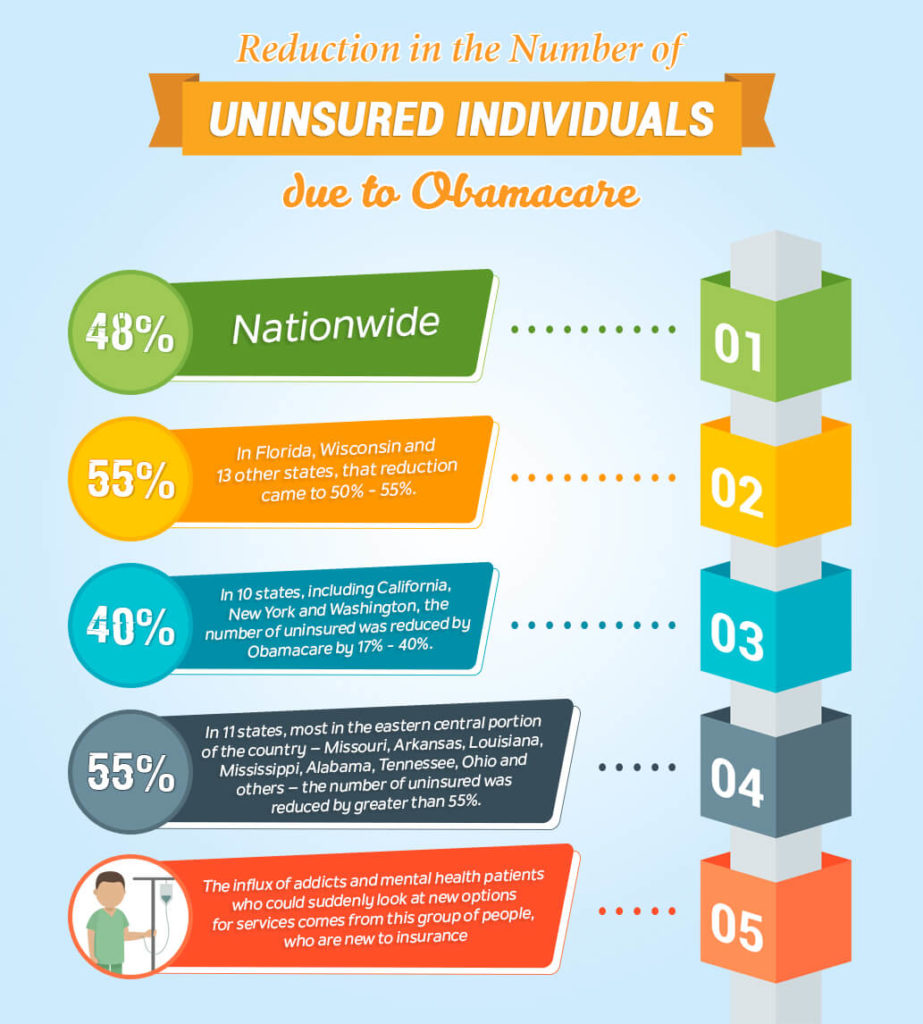

In short, this looks like every state is out for itself regarding recovery services. However, there are two sets of data that could be useful to keep in mind in this respect. First is the state by state percentage reduction in the number of uninsured individuals, which nationally stands at 48 percent.

More specifically, in Florida, Wisconsin and 13 other states, that reduction came to somewhere between 50 percent and 55 percent. In 10 states, including California, New York and Washington, the number of uninsured individuals was reduced by Obamacare by 17 percent to 40 percent. In 11 states, most in the eastern central portion of the country – Missouri, Arkansas, Louisiana, Mississippi, Alabama, Tennessee, Ohio and others – the number of uninsured was reduced by greater than 55 percent. The influx of addicts and mental health patients who could suddenly look at new options for services comes from this group of people, who are new to insurance.

Another useful statistic, found at Obamacare Facts, is how many Obamacare recipients in each state have received financial assistance with their premiums. Across the country, that figure stands at 86 percent. If subsidies or tax credits end, that many people will be affected and may have to return to not having insurance.

That figure implicates seven states above the rest – Alabama, Alaska, Florida, Louisiana, Mississippi, North Carolina and Wyoming, where more than 90 percent of those enrolled through government exchanges are receiving help with their monthly bills – including a high of 94.2 percent in Mississippi. But many other states are not far behind with an additional 16 states sporting percentages above 85 percent. The dollar figure is also shattering: The average financial assistance provided to Obamacare participants who receive help comes to $291 per month.